British Columbia Loan Agreement Template & Guide

British Columbia Loan Agreement is a simple legal document that records a promise to repay money. It protects both the lender and the borrower by clearly writing down the terms.

If you lend money to a friend, employee, or small business, things can go wrong without written proof. In real life, many disputes happen because people “assumed” terms instead of writing them. A proper agreement helps avoid confusion and keeps you legally safe in British Columbia.

I’ve seen lenders in British Columbia struggle to recover even small personal loans because nothing was written down clearly at the start. When repayment dates, interest, or missed payment terms are vague, simple loans between friends or family can quickly turn into stressful legal disputes.

A loan agreement is a written promise where one person gives money and the other agrees to repay it under certain terms.

For example, you might lend $5,000 to a friend to start a small shop. Without a written agreement, it becomes difficult to prove repayment terms later.

Under British Columbia law, a properly written contract is much easier to enforce than a verbal promise.

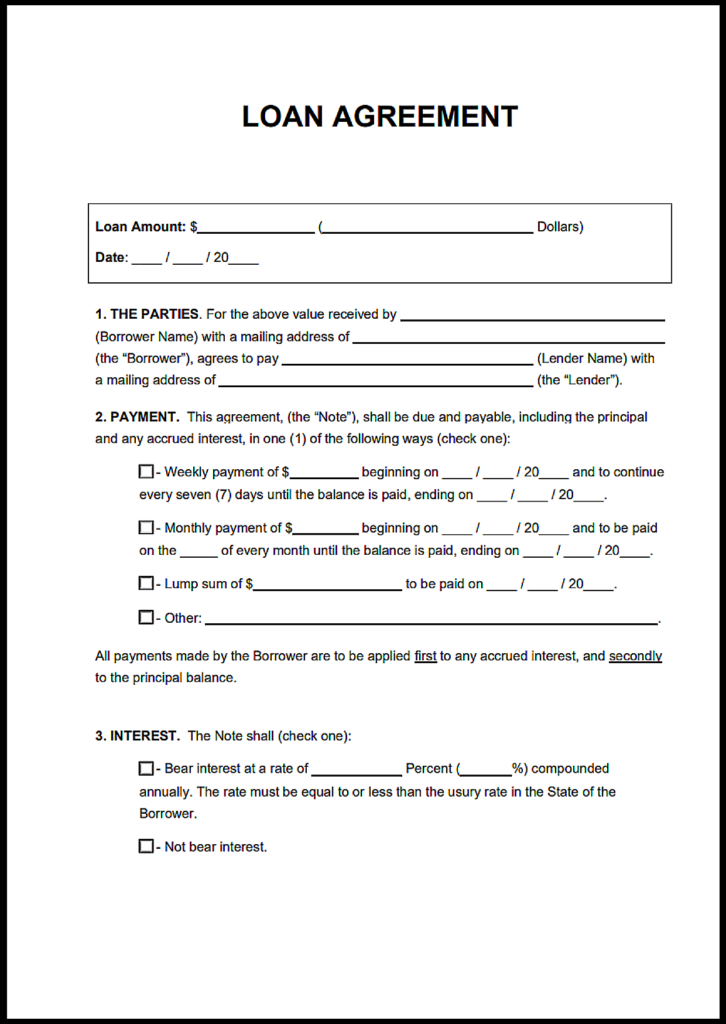

Free British Columbia Loan Agreement Template

Below is a simple, ready-to-use template. You can copy, edit, and use it based on your situation.

Important British Columbia Loan Agreement Laws You Should Know

| Topic / Issue | [British Columbia] Legal Rule | Governing Statute |

|---|---|---|

| Governing Consumer Credit Law | Consumer loan disclosure rules are governed by provincial consumer protection legislation. | Business Practices and Consumer Protection Act [SBC 2004] c. 2 |

| Federal Interest Rate Rules | Federal law controls annual interest disclosure and criminal interest rate limits. | Interest Act (R.S.C., 1985, c. I-15); Criminal Code of Canada, s. 347 |

| Age Requirement | A person must be at least 19 years old in British Columbia to properly enter most loan agreements. | Age of Majority Act, s. 1; Infants Act, s. 19 |

| Corporate Signing Authority | Corporations may sign through an authorized representative. | Business Corporations Act, s. 146 |

| Witness Requirement | Witnesses are not legally required, although commonly used for proof purposes. | N/A |

| Notarization Requirement | Notarization is generally not required unless real property is involved. | N/A |

| Mental Capacity | Adults are presumed capable if they understand the nature and consequences of the loan. | Adult Guardianship Act, s. 3 |

| Debt Claim Time Limit | Most debt recovery claims must be started within 2 years after default is discovered. | Limitation Act, s. 6 |

| Cost of Borrowing Disclosure | Consumer lenders must clearly disclose loan costs, interest, and non-interest charges. | Business Practices and Consumer Protection Act, s. 84 |

| Interest Rate Disclosure Rule | If interest is not written as an annual rate, it may legally default to only 5% annually. | Interest Act, s. 4 |

| High-Cost Credit Disclosure | High-interest loans may require cancellation rights and special disclosure language. | Business Practices and Consumer Protection Act, s. 112.06 |

| Secured Loan Registration | Lenders should register secured interests involving personal property in the BC PPR. | Personal Property Security Act, s. 25 |

| Real Estate Security Registration | Mortgage-related loan security must be registered with the LTSA. | Land Title and Survey Authority of British Columbia |

| Criminal Interest Limit | Interest above 60% effective annual rate may make the agreement illegal. | Criminal Code, s. 347 |

| Unconscionable Agreements | Courts may set aside unfair loans where borrowers were taken advantage of. | Business Practices and Consumer Protection Act, s. 8 |

| Minor Borrowers | Loan agreements with borrowers under 19 may be unenforceable unless for necessaries. | Infants Act, s. 19 |

| BC-Specific Cooling-Off Rights | Some high-cost loans include mandatory cancellation periods in British Columbia. | Business Practices and Consumer Protection Act |

| Recent High-Cost Credit Amendments | New high-cost credit licensing and disclosure rules came into force as recently as May 1, 2022. | Business Practices and Consumer Protection Act amendments (2019, 2021, 2022 changes) |

British Columbia has several loan rules that surprise many people, especially the age requirement. In BC, someone must generally be 19 to properly enter a loan agreement, unlike provinces such as Ontario or Alberta where the age is 18. This becomes important when lending money to young adults because the agreement may later become difficult to enforce.

Another major rule involves interest rates. Under Canadian criminal law, charging more than 60% annual interest can make the loan illegal. Even smaller mistakes can create problems. For example, if the agreement does not clearly explain the annual interest rate, federal law may reduce enforceable interest to only 5% annually.

The 2-year limitation period is also critical. If a lender waits too long after default, they may lose the legal right to recover the money through court action. Secured loans also require proper registration in British Columbia to protect the lender’s priority rights over collateral.

To avoid these costly mistakes, download the free British Columbia Loan Agreement template below and customize it properly for your situation.

What Is a Loan Agreement and When Do You Need One?

A loan agreement is a legal contract between a lender and a borrower. It clearly explains how much money is given and how it will be repaid.

You may need one in situations like:

- Lending money to friends or family

- Funding a small business startup

- Giving an employee a loan

- Providing short-term financial help

In most business contract situations, relying on verbal agreements is risky. People may forget details or disagree later. A written agreement removes that uncertainty.

Financial agreements are commonly connected with other business documents depending on the transaction structure. Companies working with outside service providers may also use a service agreement template, while businesses entering long-term collaborations often require a partnership agreement.

Is a Loan Agreement Legally Valid in British Columbia?

Yes, a loan agreement is legally valid in British Columbia if it meets basic contract rules.

Under British Columbia law, a contract must include:

- Offer and acceptance (both parties agree)

- Consideration (money is exchanged)

- Clear terms (repayment, interest, etc.)

- Signatures

Written agreements are not always legally required, but they are strongly recommended because they are easier to prove in court.

Key Elements of a Strong Loan Agreement

A good agreement is clear, complete, and fair.

Loan Amount and Purpose

Always mention the exact loan amount in Canadian dollars.

You can also include the purpose, such as personal use or business investment.

Interest Rate and Legal Limits

You may charge interest, but it must follow Canadian law.

The rate should be clearly written and reasonable.

Repayment Schedule

State how and when payments will be made:

- Monthly installments

- Weekly payments

- Lump sum at the end

Security (Secured vs Unsecured Loan)

Some loans are backed by assets, while others are based on trust.

Default and Penalties

Explain what happens if the borrower fails to pay:

- Late fees

- Legal action

- Asset recovery (if secured)

Signatures and Witnessing

Both parties must sign the agreement.

A witness or notarization is optional but adds extra protection.

When sensitive financial information is shared during negotiations, parties sometimes include a confidentiality agreement to help protect private business records and repayment details.

Secured vs Unsecured Loans in British Columbia

Understanding this difference is important before drafting your agreement.

| Feature | Secured Loan |

Unsecured Loan

|

| Risk for lender | Low | High |

| Collateral required | Yes | No |

| Example | Car loan | Loan to a friend |

| Legal protection | Strong | Limited |

A secured loan is safer for the lender because it is backed by an asset.

An unsecured loan is easier for the borrower but carries more risk for the lender.

How to Fill Out the Loan Agreement (Step-by-Step)

Filling the template correctly is very important.

Step 1: Add correct legal names

Use full legal names as shown on official documents.

Step 2: Clearly mention loan amount

Write the exact amount in CAD to avoid confusion.

Step 3: Decide interest and repayment

Agree on interest rate and payment schedule before signing.

Step 4: Add payment method

Mention how payments will be made, such as bank transfer or cheque.

Step 5: Review and sign

Both parties should carefully review the agreement before signing.

Tip: Always use simple and clear language. Avoid complex terms.

A secured loan is safer for the lender because it is backed by an asset.

An unsecured loan is easier for the borrower but carries more risk for the lender.

How to Fill Out the Loan Agreement (Step-by-Step)

Filling the template correctly is very important.

Step 1: Add correct legal names

Use full legal names as shown on official documents.

Step 2: Clearly mention loan amount

Write the exact amount in CAD to avoid confusion.

Step 3: Decide interest and repayment

Agree on interest rate and payment schedule before signing.

Step 4: Add payment method

Mention how payments will be made, such as bank transfer or cheque.

Step 5: Review and sign

Both parties should carefully review the agreement before signing.

Tip: Always use simple and clear language. Avoid complex terms.

Interest Rates and Legal Rules in Canada

In Canada, interest rates are regulated by law.

| Rule | Explanation |

| Maximum interest |

Cannot exceed 60% annually (Criminal Code)

|

| Transparency |

Terms must be clearly stated

|

| Fairness |

Unfair rates can make agreement invalid

|

Charging extremely high interest can make the agreement illegal. Always keep terms fair and reasonable.

Tax Implications of Loans in British Columbia

Loans can have tax effects depending on the situation.

- Personal loans: Usually not taxable

- Business loans: Interest may be taxable income

- Interest-free loans: May raise concerns with tax authorities

If the loan is large or business-related, it is wise to consult an accountant.

Common Mistakes to Avoid

Many people make simple mistakes that cause problems later.

- Not writing clear repayment terms

- Charging illegal interest rates

- Missing a default clause

- Mixing personal and business loans

- Not keeping proper records

Avoiding these mistakes can save time, money, and stress.

What Happens If the Borrower Does Not Repay?

If the borrower fails to repay, the lender has several options.

- Send reminders and try to negotiate

- Issue a written notice

- Take legal action (such as small claims court)

In British Columbia, having a written agreement makes it much easier to prove your case and recover money.

Loan Agreement vs Promissory Note

These two documents are similar but not the same.

| Feature | Loan Agreement |

Promissory Note

|

| Detail level | Detailed | Simple |

| Legal strength | Strong | Moderate |

| Use case | Business or complex loans |

Simple personal loans

|

A loan agreement is better for detailed arrangements, while a promissory note works for simple promises.

Frequently Asked Questions

Do I need a lawyer for a loan agreement in BC?

No, not always. For simple loans, you can use a template. For large or complex loans, legal advice is recommended.

Can I charge interest on a personal loan?

Yes, but it must follow Canadian laws and stay within legal limits.

Is a verbal loan agreement valid?

It can be valid, but it is difficult to prove. Written agreements are much safer.

Can I change terms after signing?

Only if both parties agree and sign the updated terms.

What if borrower refuses to sign?

If there is no signed agreement, it becomes difficult to enforce repayment legally.