Ontario Loan Agreement Template | Free Download & Legal Guide

Ontario Loan Agreement is the safest way to protect your money when lending to someone—whether it’s a friend, family member, or business partner.

Imagine lending $5,000 CAD to a friend. Everything feels fine—until repayment gets delayed or denied. Without a formal written agreement executed in compliance with the Ontario Evidence Act, proving the exact parameters of the debt obligation can become an evidentiary nightmare in a court of law.

I’ve seen Ontario lenders lose thousands because they relied on text messages or verbal promises that were impossible to properly enforce later. In Ontario, private loan defaults up to a maximum threshold of $35,000 CAD fall under the jurisdiction of the Small Claims Court pursuant to O. Reg. 626/00 of the Courts of Justice Act. Without explicit written terms detailing the dynamic of repayment, simple interpersonal advances are frequently mischaracterized as gifts, frustrating recovery attempts.

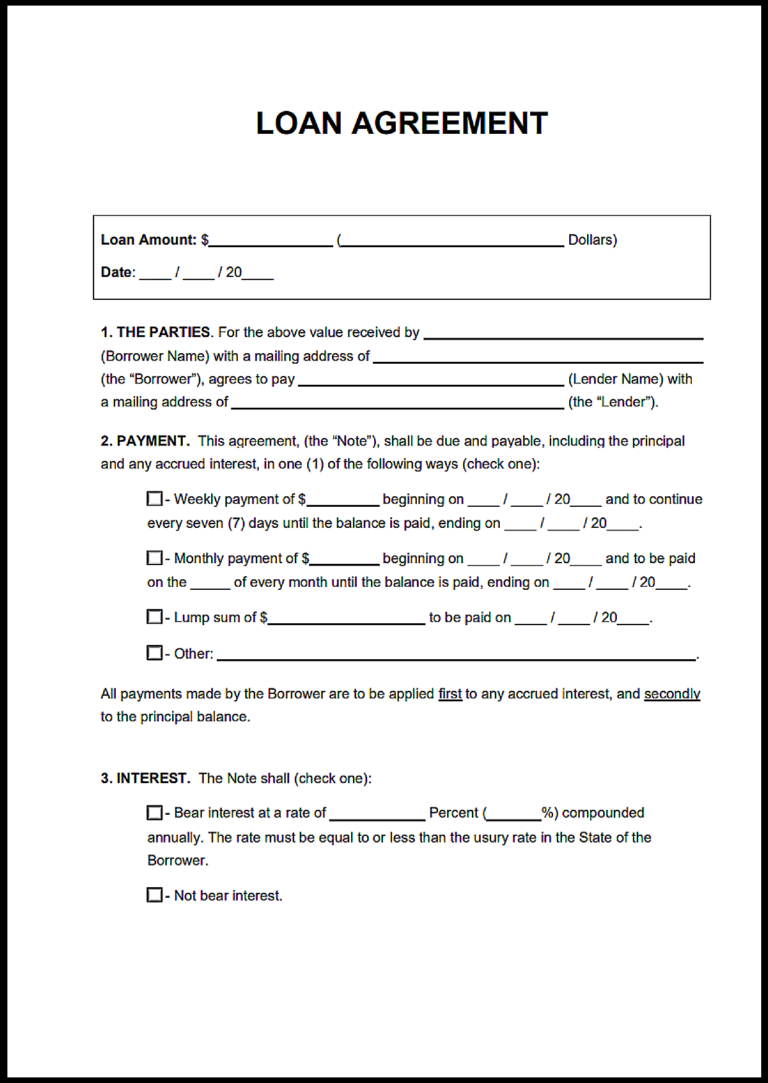

Free Ontario Loan Agreement Template

Below is a simple and practical template you can use right away. Just fill in the details.

Tip: Always keep a signed copy for both parties. Digital and physical copies are both helpful.

Ontario Loan Agreement Laws and Borrowing Rules You Should Know

| Topic / Issue | Ontario Legal Rule | Governing Statute |

|---|---|---|

| Federal interest regulation | Interest disclosure and calculation rules are governed federally. | Interest Act, RSC 1985, c I-15 |

| Consumer loan protection | Personal, family, and household loans are governed by Ontario consumer protection law. | Consumer Protection Act, 2023, SO 2023, c 23, Sch 1 |

| Commercial loan governance | Commercial lending is mainly governed through provincial commercial law and common law principles. | Mercantile Law Amendment Act, RSO 1990, c M.10 |

| Recent consumer law reform | Ontario modernized rules on unfair practices and unconscionable representations in credit agreements. | Consumer Protection Act, 2023 |

| Who can sign | Any individual with legal capacity or authorized corporate signing officer may sign a loan agreement. | Business Corporations Act, RSO 1990, c B.16 |

| Witness requirement | Witnesses are generally not legally required unless the agreement is executed as a deed or tied to land security. | Conveyancing and Law of Property Act, RSO 1990, c C.34 |

| Notarization requirement | Loan agreements generally do not require notarization unless registration or filing is involved. | Notaries Act, RSO 1990, c N.6 |

| Minimum age requirement | Contracts signed by minors (under 18) are generally voidable at the minor’s option unless for life necessities; full capacity attaches at 18. | Age of Majority and Accountability Act, R.S.O. 1990, c. A.7, s. 1 |

| Mental capacity requirement | Contracts are voidable if a party lacks the capacity to understand the agreement’s nature and consequences, and the other party knew or ought to have known of the incapacity. | Presumption of capacity under Mental Health Act, R.S.O. 1990, c. M.7, s. 2; supplemented by Ontario common law |

| Deadline to sue for unpaid debt | Lawsuits usually must begin within 2 years after the debt is discovered in default. | Limitations Act, 2002, SO 2002, c 24, Sched B, s. 4 |

| APR disclosure requirement | Consumer credit agreements must clearly state the Annual Percentage Rate (APR). | O. Reg. 17/05 under the Consumer Protection Act |

| Cost of borrowing disclosure | Agreements must disclose the total cost of borrowing, including fees and interest. | O. Reg. 17/05 under the Consumer Protection Act |

| Borrower prepayment rights | Non-mortgage consumer loans must allow full prepayment without penalty. | O. Reg. 17/05 under the Consumer Protection Act |

| Annual interest disclosure rule | If interest is calculated monthly or daily, the annual equivalent rate must be disclosed. | Interest Act, RSC 1985, c I-15, s. 4 |

| Filing requirements for unsecured loans | Private unsecured loans do not require registration. | Governed by common law principles |

| Registration of secured loans | Secured lenders should register a Financing Statement through Ontario PPSR to protect their security interest. | Personal Property Security Act, RSO 1990, c P.10 |

| Criminal interest rate limit | Interest rates above 60% annually may make the agreement or interest provision illegal. | Criminal Code of Canada, RSC 1985, c C-46, s. 347 |

| Unconscionable lending practices | Courts may set aside agreements where borrowers were unfairly taken advantage of. | Consumer Protection Act, 2023, s. 9 |

| Failure to disclose annual interest | Lenders who fail to disclose the annual equivalent rate may be limited to charging only 5% yearly interest. | Interest Act, RSC 1985, c I-15, s. 4 |

| Ontario’s strict limitation period | Ontario strictly applies a 2-year deadline to sue after default unless payment or acknowledgment occurs. | Limitations Act, 2002 |

| Ontario PPSR registration system | Ontario uses a specific electronic PPSR registration system with detailed data field requirements. | Personal Property Security Act |

| Ontario consumer protection scope | Ontario consumer lending laws require detailed disclosure and strong borrower protections. | Consumer Protection Act, 2023 |

One of the most important rules in Ontario loan agreements is the mandatory interest disclosure required under section 4 of the federal Interest Act, R.S.C. 1985, c. I-15. If a loan agreement provides for a rate of interest for any period less than a year (such as monthly or daily calculations), the agreement must explicitly state the equivalent annual rate. Failure to include this exact annual projection strips the lender of their contractually agreed rate, capping recoverable interest at a statutory default of 5% per annum.

Another major issue is Ontario’s strict 2-year limitation period for unpaid debts. Once that period passes without payment or written acknowledgment, recovering the money through court can become extremely difficult. This rule catches many informal lenders by surprise, especially in loans between friends or family members.

The criminal interest rate framework introduces severe liability for unwary private lenders. Under section 347 of the Criminal Code and the Criminal Interest Rate Regulations (SOR/2024-114), the maximum allowable rate for personal or consumer loans is strictly capped at an Annual Percentage Rate (APR) of 35%. Lenders must explicitly calculate and disclose the APR to ensure compliance with both federal criminal law and the disclosure protocols of the Consumer Protection Act, 2002. Exceeding this 35% APR threshold renders the interest provision void ab initio as illegal and exposes the lender to criminal prosecution. Download the free Ontario Loan Agreement template below to create a clearer and legally compliant lending agreement.

Understanding Ontario Loan Agreements

What Is an Ontario Loan Agreement?

An Ontario loan agreement is a legal contract where:

- One person lends money

- Another person agrees to repay it under clear terms

Under Ontario law, this applies to:

- Personal loans (friends/family)

- Business loans

- Private lending arrangements

Verbal vs Written Agreements

A verbal agreement can be valid, but it’s risky.

| Type | Risk Level | Proof |

| Verbal Agreement | High | Hard to prove |

| Written Agreement | Low |

Clear legal evidence

|

A written agreement removes confusion and protects both sides.

When Should You Use a Loan Agreement?

Use it anytime money is involved, especially:

- Lending to friends or family

- Funding a startup or business

- Employee loans

- Private lending deals

Real-life example:

You lend $5,000 to a friend. No agreement, no repayment date. After 6 months, they say, “I thought it was a gift.”

Now you have no proof—this happens more often than you think.

Is a Loan Agreement Legally Enforceable in Ontario?

Yes—if it meets basic contract law rules:

- Offer → One party offers the loan

- Acceptance → The other agrees

- Consideration → Money is exchanged

A contract is legally binding when all three exist and terms are clear.

When it may NOT be enforceable:

- No signatures

- Vague repayment terms

- Illegal interest rates

- Missing key details

While loan agreements focus on financial terms, in some cases confidentiality clauses may apply, which are explained in the Ontario NDA template guide.

Key Terms Every Ontario Loan Agreement Must Include

Loan Amount and Currency

Always write the amount clearly in Canadian Dollars (CAD).

Interest Rate (and Legal Limits)

Under section 347 of the Criminal Code of Canada and the Criminal Interest Rate Regulations (SOR/2024-114), charging an Annual Percentage Rate (APR) exceeding 35% constitutes a criminal offense for consumer and personal loans.

Keep interest:

- Reasonable

- Clearly written

- Easy to calculate

Repayment Schedule

Choose one:

- Lump sum (one payment)

- Installments (monthly/weekly)

Always include exact dates.

Default and Late Fees

Explain:

- What happens if payment is late

- Any penalties or extra fees

Security (Optional)

- Secured loan → backed by an asset (car, property)

- Unsecured loan → based on trust

Governing Law Clause

Always include:

“This agreement is governed by the laws of Ontario.”

Secured vs Unsecured Loans

| Type | Meaning | Risk |

| Secured Loan | Backed by asset |

Lower risk for lender

|

| Unsecured Loan | No collateral | Higher risk |

Example:

- Secured → Borrower gives car as collateral

- Unsecured → No asset, only promise

Key insight:

If the borrower defaults, secured loans give you a way to recover money.

How to Fill Out the Ontario Loan Agreement

Follow this simple process:

Step 1: Add Names and Addresses

Use full legal names and correct addresses.

Step 2: Define Loan Amount and Interest

Be exact. Avoid vague numbers.

Step 3: Choose Repayment Structure

Decide:

- One-time payment OR

- Installments

Step 4: Add Clear Dates

Include:

- Loan start date

- Repayment dates

Step 5: Sign the Agreement

Both parties must sign.

Important tip:

Each person should keep a signed copy.

This document can also relate to a partnership agreement or a contract drafting guide when structuring more complex financial arrangements.

Common Mistakes to Avoid

Many people lose money due to simple errors:

- No repayment dates

- Illegal or unclear interest rates

- Not signing the agreement

- Using vague language

- Ignoring default clauses

Practical tip:

If something feels “understood,” write it down anyway.

Legal Risks of Not Using a Loan Agreement

Skipping a written agreement can lead to:

- No proof in disputes

- Difficulty recovering money

- Damaged relationships

- Court challenges

Scenario:

A business owner lends $10,000 to a partner. No contract. The partner leaves and refuses to repay.

Without written proof, recovery becomes very difficult.

Interest Rates and Canadian Law

Under the Criminal Code of Canada, s. 347, and the Criminal Interest Rate Regulations (SOR/2024-114):

-

Consumer/Personal Loans: Charging an interest rate exceeding an Annual Percentage Rate (APR) of 35% is a criminal offense.

-

Commercial Loans: Loans between $10,000 and $500,000 are capped at 48% APR; commercial credit advances exceeding $500,000 are entirely exempt from the criminal rate framework.

Why this matters:

The definition of ‘interest’ under s. 347(2) is exceptionally broad, capturing all fees, administrative charges, bonuses, and penalties. If your calculated APR crosses the 35% threshold on a personal loan, the entire interest clause is severed as illegal, meaning you lose the legal right to collect any interest whatsoever.

Keep interest:

- Fair

- Transparent

- Clearly written

Loan Agreement vs Promissory Note

| Feature | Loan Agreement |

Promissory Note

|

| Detail Level | High | Low |

| Legal Protection | Strong | Limited |

| Best Use | Complex loans | Simple loans |

Use a loan agreement when:

- Large amount involved

- Multiple conditions exist

Use a promissory note for simple repayment promises

You can also explore our Ontario Promissory Note template for simpler lending situations.

FAQs About Ontario Loan Agreements

Do I need a lawyer to create a loan agreement?

No, you don’t always need a lawyer for a loan agreement. For simple loans, a clear written template works well, but for large or complex deals, legal advice is recommended.

Can I lend money without interest in Ontario?

Yes, you can lend money without charging interest. Many personal or family loans in Ontario are interest-free and still legally valid.

Is a handwritten loan agreement valid?

Yes, a handwritten loan agreement is valid if it is signed, the terms are clearly written, and both parties fully agree to the conditions.

What happens if the borrower doesn’t pay?

If the borrower does not repay, you can enforce the agreement. You may also take legal action or claim damages through the court.

Can I change the agreement later?

Yes, you can change the agreement later, but both parties must agree to the changes and sign the updated version to make it valid.